Strong euro a focus as bankers discuss inflation target

- Serie A | Udinese VS Inter Milan; Tuesday, 09 April at 02:45 GMT +8

- Man Utd VS Manchester City || Sunday, 29 October at 23:30 GMT +8

- Người đàn ông đứng đằng sau chiến tích lịch sử của ĐTQG U23 Việt Nam tại Asiad

Five big themes likely to dominate thinking of investors and traders in the coming week.

- Money talk

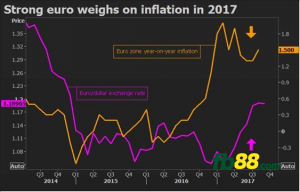

The strength of the euro is likely to be the main discussion point at Thursday’s European Central Bank meeting, as policymakers weigh up what it means for their inflation target and how quickly they can scale back stimulus. There has been a dramatic shift in expectations for central bank announcements recently. A survey on Friday showed a quarter of economists polled by Reuters expect the ECB to announce a change to its asset purchase program on Thursday, down from over half three weeks ago. The main culprit is the euro, which with all the uncertainty generated by everything from Brexit to Trump to North Korea, is emerging as a safe-haven currency. The single currency’s strength is now very much part of the internal debate within the ECB, sources said, as it makes imports to the bloc cheaper and holds down consumer prices. Euro zone inflation rose slightly more than forecast in August to 1.5%, but it is well short of the ECB’s target and a four-year peak of 2% struck in February.

- Sealing a deal?

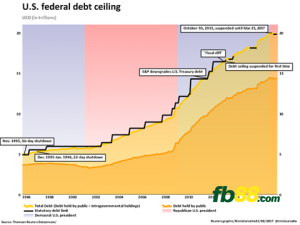

Investors will be hoping for a swift resolution to a looming deadline to raise the US debt ceiling, which stands at about $19.8 trillion. While Congressional Republicans have not spelled out their plan for dealing with an annual spending bill deadline, and the increase in the federal debt ceiling, some have speculated those issues might be swept into one piece of legislation, possibly including Harvey aid.

US Treasury Secretary Steven Mnuchin on Thursday told CNBC he would be open to the debt limit being dealt with as part of a Harvey relief bill, although he said spending on the hurricane could bring forward the debt ceiling deadline. The last major standoff over lifting the debt ceiling, in mid-2011, ultimately cost the United States its prized triple-A credit rating from Standard & Poor’s and came close to tipping US stocks into a bear market. In the 11 trading days that marked the height of the crisis, the S&P 500 fell 16.7% – its sharpest decline over any comparable period since the 2007-2009 financial crisis.

- Emerging stronger

Emerging market equities are topping the global performance league tables this year, with dollar-based returns of more than 26%. The MSCI index has just recorded it eighth straight month of gains in August, the best run since 2003-04. There is likely more to come. Markets are pricing out another Fed rate rise by year-end, keeping the dollar in check. US President Donald Trump has not managed to deliver any stimulus. Emerging and developing economies are recovering steadily –surveys show factory production and exports roared ahead in China and almost everywhere else last month.

Finally, emerging companies have surpassed earnings expectations by roughly 2.6% the latest quarter, Morgan Stanley estimates, with Chinese firms leading the pack with an 8.2% beat. This is shaping up to be the best year for the MSCI EM index since 2009. But that year, with returns of 70%-plus fuelled Fed money printing, may prove too hard to beat.

- Powerful backing

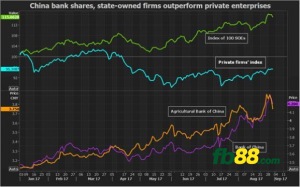

“When the state sector advances, the private sector retreats” – so goes the Chinese idiom. China’s push this year with supply-side reforms to kill excess capacity and wean its economy off debt certainly appear to be having that effect, handing its mammoth state-owned sector a massive advantage in costs and opportunities and starving the private sector of both cash and profits. The outperformance of the stock market sub-indices of state-owned firms over the private sector index attests to that. Profits at China’s state-owned enterprises (SOEs) were up 44.2% between January and July from a year earlier, triple the pace of the 14.2% rise in private sector profits.

China’s big four banks, including Bank of China, are at the fore of this outperformance and reform drive that have sent their margins soaring and raised hopes of an improvement in loan quality. The launch of new funds by the government dedicated to financing SOE reform, coming ahead of the Communist Party’s 19th Party Congress, should only extend that advantage.

- Laboring stocks

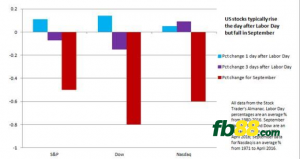

US investors typically return from the long Labor Day weekend refreshed and ready to buy. The day after the holiday, the S&P 500 gained 0.1% on average between 1980 and 2016, according to the Stock Trader’s Almanac. But that’s where the optimism typically ends. September as a whole is the worst month in the year for stock performance, with the S&P falling on average 0.5%. This September could be particularly nail-biting. Wall Street may be facing a rough ride if there is a showdown in Washington over the US budget and the federal debt ceiling. Meanwhile, North Korea is an concern, as is the impact of Harvey. The potential headwinds come against a particularly optimistic market: the S&P 500 is up 10% this year, with the 12-month forward P/E ratio at 17.5 versus an all time average of 15.